While there are few who will disagree that electric vehicles will form a greater proportion of vehicle fleets going forward, who will dominate and what technologies will come to the forefront is less clear.

According to research by IDTechEx, newcomers to the automotive space are set to dominate in electric vehicles if the traditional automotive leaders don’t begin responding to the opportunity/threat soon.

The organization’s recent report drilled down into the prospective landscape going forward for electric vehicles

Fuel cells are losing the battle in most mobility segments

It is clear to IDTechEx that fuel cells have few opportunities in light and medium-duty mobility segments, and 2019 cements this. The main problem fuel cells face competing with batteries is additional and highly inefficient energy-conversion steps: first converting water to H2 with electricity, and then the fuel cell itself is roughly 60% efficient when converting H2 back to electricity and water for the vehicle (large heat losses). As a result, fuel cells need an abundance of renewable energy to operate cleanly, which in itself will be a challenge.

Moreover, fuel cell vehicles still need a sizable battery for high-power and energy harvesting; they have moving parts (= maintenance); hydrogen charging infrastructure costs many multiples that of a fast charger; they rely on expensive raw materials; there is no roadmap to economies of scale, and so on.

Three new nails were placed in the coffin of fuel cell vehicles in 2019:

- China issued a statement that the fuel cell subsidy will not remain in place beyond 2020, reflecting that progress with fuel cells is very poor, despite financial incentives.

- Fuel cells are losing opportunities in heavy-duty segments: approaching half of European pure electric buses use top-up charging by gantries or intermittent non-stop charging with bits of catenary. This means a smaller (cheaper) battery is needed, making fuel cells less competitive.

- The head of VW Group (auto number one) said serious inefficiency of fuel cells denies them a place in its agenda.

It is of note, however, that Toyota has prioritized fueled vehicles in the form of fuel cell and hybrid versions, mainly with cars.

However, fuel cells have had some positives this year: Hyundai announced a fuel cell truck, and Nikola announced impressive partnerships along with 14,000 pre-orders.

However, the positives generally reflect the wider trend that fuel cells are only competitive in long-haul heavy-duty segments. And this is just for now — even here there will be tough competition with batteries (Tesla Semi).

Newcomers made the running in what matters

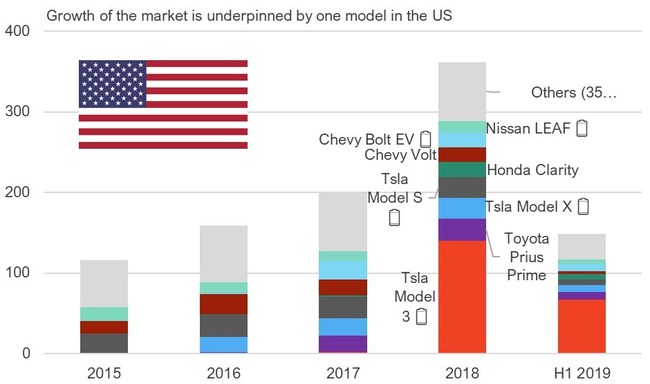

In 2019, newcomers made most of the running with pure electric vehicles that are rapidly becoming the only show in town. Tesla stormed ahead in a declining car market, underpinning growth in the US and Europe by selling vehicles the giants still do not offer (see chart).

Indeed, VW Group executives admitted they lack the skills as yet (and admitted that Tesla is no longer at risk financially). Elon Musk pointed out that the Audi e-tron and Mercedes equivalent in 2019 turned out to be copies of six-year-old Teslas. He was being kind. With no attempt at Tesla streamlining, their inferior drag factor and lack of the latest Tesla motor efficiency led to inferior range, with sales to prove it. Range sells cars. Long range pure electric vehicles have three times the resale value.

To the eternal shame of the giants, even the more futuristic start-ups made a giant splash: Sono Motors took over 10,000 orders for its all-over solar car (= $200 million), and start-up Lightyear took over $10 million in orders for its high-priced, advanced solar cars (with record range for any production car, and with half the typical battery size). Beyond conformal solar technology, Lightyear also showed-off how to make axial flux in-wheel motors with a record power-to-weight ratio.

Despite these wins, it is still a serious challenge moving from prototypes and hype to serial production. Thus far, Tesla is the only survivor. Sono needs to raise 255 million euros ($250 million) to get to production: in order to continue, they need 50 million euros ($56 million) by the end of 2019.

The response

VW Group continued its U-turn, promising to invest more in pure electric vehicles than any other company on Earth. It published figures showing it would grab 20% of planned global battery production in the process. However, it remains to be seem if it can make vehicles people want to buy in the necessary large numbers.

Hyundai showed modernity with excellent pure electric cars below Tesla price segments, getting excellent order books. It is also the first OEM to offer a large solar roof on a production car. Light users will get 10% of their electricity on Sonatas in S Korea. Hyundai additionally promises a large solar roof on pure electric Hyundais and Kias, including a translucent one.

Newcomers grab the truck market

Tesla immediately took 250,000 pre-orders of cybertrucks in the first week (= more than $10 billion), treading on Rivian’s toes (Rivian earlier took 100,000 orders of tailored pure electric delivery trucks from Amazon).

The true test for both Rivian and Tesla will be the entry of Ford into the electric pickup market. With Rivian’s R1T pickup scheduled to begin deliveries in late 2020, and the Tesla Cybertruck set to roll off the assembly line in late 2021, Ford has been stirred into action and are now promising an electric version of their Ford F-Series by 2022 (which made up 30.8% of US pickup sales in 2018). Having been slow to act on the rise of EV, Ford’s all-electric F150 could be a game changer.

It gives Rivian and Tesla only a short window to establish a market share before the pickup market behemoth enters with its incumbent advantages in volume production expertise, economy-of-scale, loyal customer base and established dealer network. Whether Ford can reach EV technology parity in the short-term is the test for them, and they may be forced to purchase their way there.

Meanwhile, back at the ranch, Daimler (world number one in trucks) has been realizing it will face the same future in trucks as with its buses, where it tumbled from leadership. Announcing a layoff of 10,000 people this year, it will not participate in the new form of transportation called the robot shuttle.

Sensibly, Hyundai has gone into buses and Tesla may follow suit after its formidable truck entry. China’s auto giants are also in buses and trucks: a good strategy in the face of ‘peak car’. Baidu, the ‘Google of China’, collaborates with the leading Chinese bus company King Long to be one of the robot shuttle leaders by deploying over 100 of them. Indeed, none of these companies have to worry about peak car.

Against the backdrop of a car market that has declined two years in a row, the companies paying Tesla billions of dollars in emissions-credit deals look particularly fragile. Some scramble for partnerships, but combining two struggling entities rarely results in a winner.

To find out more about Electric Vehicle research available from IDTechEx visit www.IDTechEx.com/research/EV.

0 Comments